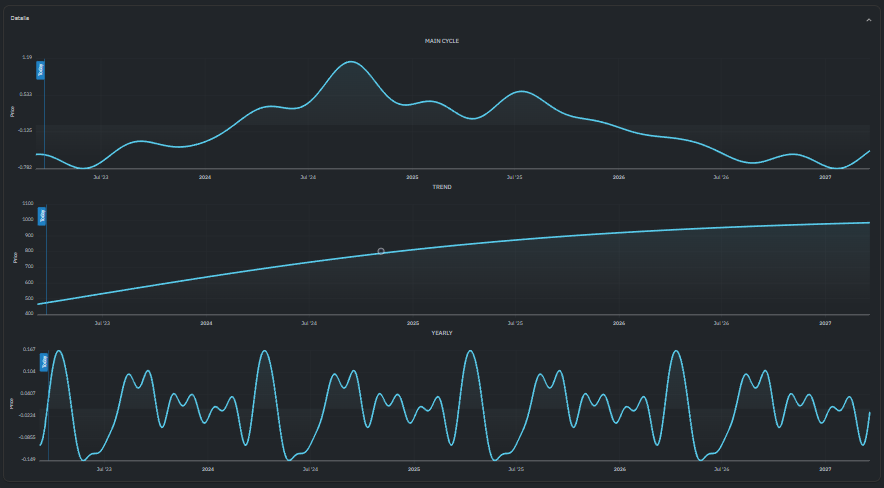

Test the AI stock trading algorithm's performance against historical data by backtesting. Here are 10 ways to determine the validity of backtesting and make sure that the results are accurate and realistic:

1. You should ensure that you have enough historical data coverage

The reason is that testing the model under different market conditions demands a huge amount of historical data.

How to: Ensure that the time period for backtesting incorporates different cycles of economics (bull markets bear markets, bear markets, and flat markets) over multiple years. This will assure that the model will be exposed in a variety of conditions, giving an accurate measurement of consistency in performance.

2. Confirm Realistic Data Frequency and the Granularity

What is the reason? Data frequency (e.g., daily or minute-by-minute) should match the model's expected trading frequency.

How: To build an efficient model that is high-frequency, you need the data of a tick or minute. Long-term models however make use of weekly or daily data. A lack of granularity could result in misleading performance information.

3. Check for Forward-Looking Bias (Data Leakage)

Why: Data leakage (using data from the future to support predictions made in the past) artificially improves performance.

What to do: Confirm that the model uses only information available at every point in the backtest. It is possible to prevent leakage using protections like time-specific windows or rolling windows.

4. Evaluate Performance Metrics Beyond Returns

Why: A focus solely on returns may obscure other risk factors.

What to do: Examine additional performance metrics such as Sharpe ratio (risk-adjusted return) as well as maximum drawdown, the volatility of your portfolio and hit ratio (win/loss rate). This will give you a complete view of the risk and consistency.

5. Assess Transaction Costs and Slippage Beware of Slippage

Why: Ignoring slippages and trading costs can result in unrealistic expectations for profits.

What to do: Check that the backtest is based on real-world assumptions about commission slippages and spreads. The smallest of differences in costs could have a significant impact on results for high-frequency models.

6. Review Position Sizing and Risk Management Strategies

The reason is that position sizing and risk control impact the returns and risk exposure.

What to do: Make sure that the model has rules for sizing positions that are based on risk (like maximum drawdowns or volatile targeting). Backtesting must take into account risk-adjusted position sizing and diversification.

7. Verify Cross-Validation and Testing Out-of-Sample

Why? Backtesting exclusively on in-sample can lead models to perform poorly in real-time, when it was able to perform well on historical data.

How: Look for an out-of-sample time period when cross-validation or backtesting to determine generalizability. Out-of-sample testing provides an indication for real-world performance when using data that is not seen.

8. Assess the Model's Sensitivity Market Regimes

Why: Market behaviour varies significantly between flat, bull and bear phases which can impact model performance.

How do you compare the outcomes of backtesting over various market conditions. A reliable system must be consistent or include adaptive strategies. Positive indicators include a consistent performance under various conditions.

9. Consider the Impact of Reinvestment or Compounding

Reinvestment strategies could overstate the return of a portfolio if they are compounded in a way that isn't realistic.

How do you ensure that backtesting is based on realistic assumptions about compounding and reinvestment strategies, like reinvesting gains, or only compounding a small portion. This method helps to prevent overinflated results due to an exaggerated strategies for reinvesting.

10. Verify the reliability of backtest results

Why is reproducibility important? to ensure that results are consistent and are not based on random conditions or particular conditions.

How do you verify that the backtesting process is able to be replicated with similar input data to produce the same results. The documentation should be able to produce identical results across different platforms or environments. This will add credibility to your backtesting method.

These guidelines will help you evaluate the quality of backtesting and improve your comprehension of an AI predictor’s potential performance. You can also assess if backtesting produces realistic, accurate results. See the top rated microsoft ai stock hints for website recommendations including ai publicly traded companies, stock technical analysis, best ai stocks to buy, ai in trading stocks, artificial intelligence and investing, artificial intelligence and investing, artificial intelligence stock market, best ai companies to invest in, stock technical analysis, top stock picker and more.

Ai Stock to learn aboutTo Discover 10 Best Tips on Strategies to assess Assessing Meta Stock Index Assessing Meta Platforms, Inc., Inc. Formerly known as Facebook Stock by using an AI Stock Trading Predictor requires knowing the company's business operations, market dynamics or economic aspects. Here are 10 top suggestions for evaluating Meta stock using an AI model.

1. Understanding the business segments of Meta

Why: Meta generates revenues from many sources, such as advertising on platforms such as Facebook and Instagram and virtual reality and its metaverse initiatives.

Learn about the revenue contribution of each segment. Understanding the growth drivers for every one of these sectors aids the AI model to make informed predictions regarding future performance.

2. Integrate Industry Trends and Competitive Analysis

Why: Meta's performance can be influenced by the trends in the field of digital marketing, social media usage as well as competition from other platforms like TikTok and Twitter.

What should you do: Ensure that you are sure that the AI model is studying relevant trends in the industry. This can include changes to advertisements as well as user engagement. Competitive analysis can assist Meta determine its position in the market and the potential threats.

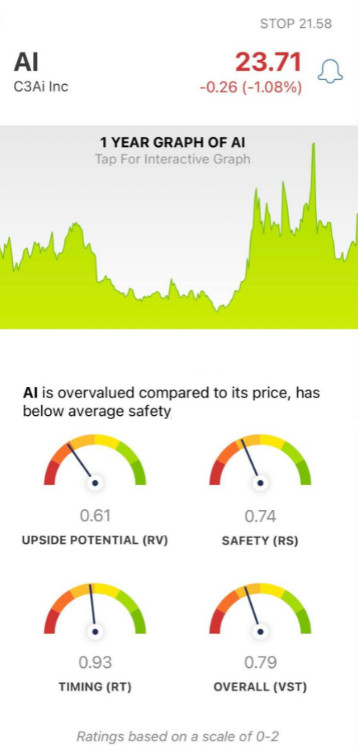

3. Earnings Reported: A Review of the Effect

Why: Earnings announcements can cause significant price fluctuations, particularly for growth-oriented companies such as Meta.

Check Meta's earnings calendar and analyze the stock performance in relation to the historical earnings unexpectedly. Investor expectations can be assessed by taking into account future guidance provided by the company.

4. Utilize for Technical Analysis Indicators

The reason is that technical indicators can identify trends and potential reversal of Meta's price.

How: Include indicators like moving averages (MA) and Relative Strength Index(RSI), Fibonacci retracement level, and Relative Strength Index into your AI model. These indicators assist in determining the best entry and exit points to trade.

5. Macroeconomic Analysis

The reason is that economic conditions such as inflation, interest rates and consumer spending can affect the revenue from advertising.

How: Ensure the model incorporates relevant macroeconomic indicators, such as employment rates, GDP growth rates data and consumer confidence indexes. This context increases the model’s predictive abilities.

6. Implement Sentiment Analysis

What is the reason? Market sentiment has a major impact on stock price, especially in tech sectors in which public perceptions matter.

Utilize sentiment analysis to gauge the opinions of the people who are influenced by Meta. These types of qualitative data can give contextual information to the AI model.

7. Keep track of legal and regulatory developments

What's the reason? Meta is subject to regulatory scrutiny in relation to data privacy, antitrust issues and content moderation, which could affect its business and stock performance.

How: Stay updated on relevant legal and regulatory changes that could affect Meta's business model. The model must be aware of the potential risks that come with regulatory actions.

8. Backtesting historical data

What is the reason: The AI model is able to be tested through backtesting using historical price changes and incidents.

How: Backtest model predictions with the historical Meta stock data. Compare predictions and actual results to determine the model’s accuracy.

9. Review Real-Time Execution metrics

Reason: A speedy execution of trades is essential to capitalizing on price movements within Meta's stocks.

How can you track key performance indicators such as fill rates and slippage. Evaluate how the AI model is able to predict the best entries and exits for trades that involve Meta stock.

Review the Position Sizing of your position and Risk Management Strategies

Why: Risk management is essential in securing the capital of investors when working with stocks that are volatile like Meta.

How: Ensure the model is incorporating strategies for positioning sizing and risk management that are based on the volatility of Meta's stock and the overall risk of your portfolio. This can help reduce the risk of losses while maximizing returns.

Follow these tips to evaluate an AI stock trade predictor’s capabilities in analysing and forecasting movements in Meta Platforms Inc.’s shares, and ensure that they are accurate and up-to-date with changing market conditions. Read the top rated microsoft ai stock hints for website advice including artificial intelligence stock trading, predict stock market, stock market ai, stock market ai, ai trading software, stock pick, best stocks for ai, good stock analysis websites, best ai stocks to buy now, ai trading apps and more.